Infralogic: How GLP is navigating China's post-subsidy energy revolution

This article was first published on Infralogic on 17 December 2025

As is typical in China, a prosaic government decree has ushered in profound change for the country's renewables sector that will see projects subject to the same market forces as most other developed markets.

For over a decade, China's renewable energy sector was one of sheer, overwhelming scale. Deploying gigawatts of solar and wind driven by state-level targets and feed-in tariffs. For investors, the model was often straightforward: secure project rights, build, and connect to the grid, with returns largely secured by policy.

The scale is still gigantic, but the era of government underwriting most of it is coming to an end.

A quiet revolution is now re-engineering the world's largest clean energy market, moving it from a top-down, capacity driven model to a more bottom-up ecosystem where, just as in many Western markets, the customer will now play a more critical role.

Navigating this requires a new playbook, and among the investors that are mapping its contours is Singaporean logistics-to-power conglomerate GLP.

"This year has been a tipping point for the entire industry," Nick Zhou, general manager with GLP Renewable Energy told Infralogic. "A lot of our peers, including the SOEs, and the private sector companies are [adjusting] their investment strategy because of Document 136."

Document 136 is a joint notice released by the Chinese authorities in early 2025 which mandates that starting from June 2025, new wind and solar projects shall, in principle, participate in the merchant power market.

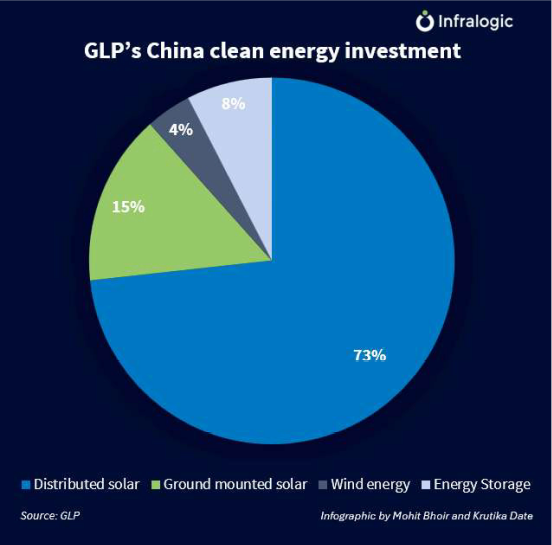

GLP has invested in China's renewable energy sector through its alternative asset management arm GLP Capital Partners (GCP), which oversees USD 79bn in assets. With a 1 GW plus portfolio encompassing distributed solar, ground-mounted solar, wind, and energy storage, the company represents one of the largest foreign investors in the country's green energy universe.

In a market characterised by both opportunity and escalating complexity, the company's strategy could offer a case study in how international capital can adapt and potentially thrive amid regulatory upheavals.

Guaranteed offtake to merchant risk

While the overarching ambition of China's energy transition - recently reaffirmed by President Xi Jinping's pledge to increase the share of the country's non-fossil fuel resources in its energy mix to 30% by 2035 - provides the "common denominator" for all investors, Zhou reckons that Document 136 may well be the specific mechanism reshaping the market.

This policy draws a line under the fixed-price, guaranteed offtake model, pushing generators to sell their electricity output at market-driven prices and directly negotiate with end-users. This timeline is seen by many as transforming the theoretical market-based reforms into an immediate operational reality for all players.

The most profound change to be brought by the new mechanism may be the shift in what determines a project's success.

The pre-Document 136 landscape was, in Zhou's assessment, "mostly a game of cost of capital." It used to be a field dominated by players with access to cheap financing, predominantly SOEs and some private developers, who could operate on relatively low required rates of return.

"The biggest [change], it's very intriguing, is that it's led renewable energy to become more customer-centric," Zhou explained, adding there could be a rebalancing of the risk and return profile of a typical project. The new model could see 70% of the overall project returns hinge on whether the developer is able to secure a power purchase agreement (PPA), he said.

To retain the client throughout the project's lifespan, the company is now providing a suite of energy solutions services that go beyond simply building projects and selling power.

"We're not competing on developing solar or wind [in a] specific province," he says. "It's more - how can you provide your off-taker with the most competitive and comprehensive energy solutions."

This involves bundling utility-scale power, distributed solar, behind-the-meter energy storage and power trading into a single, optimised package. In the meantime, it also aims to leverage GLP's inherent advantages: its portfolio of logistics parks, industrial parks and data centres in China provides built-in demand for GLP's green power plants and a test base for the integrated energy solutions.

Wind favoured

In this customer-centric investment playbook, not all projects are of equal value. GLP's current preference within the utility-scale sector hints at wind beating solar.

The rationale partially lies in the generation curve. As the market moves towards power trading, the value of electricity is no longer flat; it fluctuates hourly. "The curve matters," Zhou notes.

Wind power, with its more distributed output across the day and night, may be better positioned to capture value during higher-priced periods.

This is not a wholesale dismissal of solar, however. Viability of a power source, Zhou noted, is intensely geographical. Coastal regions with robust industrial demand and higher wholesale electricity prices remain attractive for solar investment, provided capital expenditure is tightly controlled. "With the right price evaluation, I think we can still invest without securing a client in coastal regions," he suggests, indicating a calculated comfort with merchant risk in these specific locales.

However, for projects in other provinces, where the grid is more congested and curtailment risk is historically higher, the investment thesis shifts. Here, de-risking through a pre-committed user is essential.

"For projects in the mid-to-west regions, we are looking for customer pre-commitments covering up to 70%-80% of the generation," Zhou noted. This translates into a strategy of deep customisation, working with multinational or top-tier domestic corporations that have explicit 100% green energy targets.

GLP develops a bespoke portfolio of assets for the off-taker's profile, often integrating energy storage, and using the power trading market to balance the remaining volumes, he adds.

Portfolio approach to credit risk

GLP, which owns a more than 700 MW distributed solar portfolio in China, acknowledges that a critical element for an investor to consider in the commercial and industrial (C&I) solar space is credit risk. With corporate PPAs still a developing instrument in China, Zhou notes that predicting which corporate clients will last 20 years is unrealistic.

The solution may be standardisation and portfolio diversification.

Instead of betting on any single C&I customer, it uses a standard energy management contract across a broad client base, accepting that some may fail while the overall portfolio remains profitable. Any uncontracted power can still be sold to the grid, providing a safety net.

Strategic partnerships

GLP's China's Clean Energy strategy is being executed through a multi-pronged partnership strategy with various types of investors, from China and overseas, designed to blend strategic capital with development expertise.

In 2023, GCP raised CNY 4bn (USD 554m) for its first China-focused clean energy platform from investors including the state-owned National Green Development Fund and feeder funds associated with CHN Energy Investment Group.

This partnership provides not just capital but also access to critical grid relationships and a balance sheet that can underpin larger-scale utility projects. The company's existing partnership with the SOEs could help GLP secure more project resources at a lower price, according to Zhou.

Alongside state capital, GCP is forging alliances with private sector specialists to accelerate its distributed energy footprint.

In 2023, it teamed up with Chinese private-sector solar developer PCG Power to launch a private equity joint venture. This collaboration has since borne fruit, with a green fund reaching its first close in June 2024, backed by commitments from several Chinese LPs. The vehicle aims to raise CNY 2bn and initially develop about 2.5 GW of commercial and industrial solar and distributed wind projects. Distributed solar and wind farms are projects that provide onsite power to customers.

The company last year made a decision to dissolve its 50:50 China distributed solar JV with Brookfield due to what were described as different strategic priorities, Zhou said. He noted, however, it did not signal any retreat from its renewable expansion in China.

Power storage, capital recycling next

Looking beyond the immediate horizon, Zhou identifies energy storage as a logical sector to invest in.

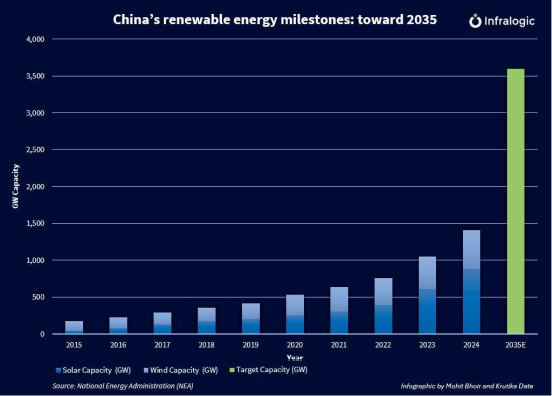

To hit the country's ambitious target of installing 3,600 GW of solar and wind projects by 2035, China must install roughly 400 GW of new renewable energy capacity per year.

"Solar is already a key component of China's renewable strategy, but it's intermittent;' he argued. "So a natural next step would be to look at energy storage assets to come alongside solar." Against an evolving policy backdrop, he sees potential for new revenue opportunities as the overall industry moves toward grid-responsive balancing and electricity trading.

On the exit front, Zhou observes a market maturing in its liquidity options. The traditional trade-sale to SOEs remains active. The development of private Real Estate Investment Trusts (REITs) and other securitisation vehicles will form additional sale channels.

"There's a huge trend on sort of the private REITs as a connection between private equity funds to the REITs. We see a lot of potential there," he notes.

This provides a potential pathway for development platforms like GLP to recycle capital by selling operational assets into yield-focused vehicles that are increasingly attractive to domestic insurance companies and pension funds.

In the longer term, Zhou believes that the ongoing reforms, while complex, could make China's renewable sector more compelling for international capital, with the market to play a bigger role in the game.

For international investors, the message is clear that the low-hanging fruit of subsidy-driven development is gone.